I. The Shock Proposal: Changing the Nature of ACA Subsidies

I. The Shock Proposal: Changing the Nature of ACA Subsidies

The recent proposal by President Donald Trump to fundamentally change how Affordable Care Act (ACA), or Obamacare, subsidies are distributed has triggered a fierce policy debate. This is not merely a healthcare reform plan but a calculated political maneuver launched right in the middle of what has become the longest federal government shutdown in US history.

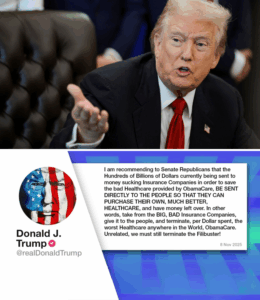

The core of the proposal is to reroute the billions of federal dollars currently paid directly to insurance companies (to lower monthly premiums for qualified individuals) and instead send those payments directly to individual Americans. Mr. Trump urged Republican Senators to act:

“I am recommending to Senate Republicans that the Hundreds of Billions of Dollars currently being sent to money sucking Insurance Companies in order to save the bad Healthcare provided by ObamaCare, BE SENT DIRECTLY TO THE PEOPLE SO THAT THEY CAN PURCHASE THEIR OWN, MUCH BETTER, HEALTHCARE, and have money left over.” (Excerpt from a Truth Social post)

He characterized the current subsidies as a “windfall for Health Insurance Companies, and a DISASTER for the American people,” suggesting that individuals could use the funds to buy better, cheaper coverage, or potentially deposit the money into tax-advantaged accounts like Health Savings Accounts (HSAs).

II. The Tense Political Context: The Shutdown and the ACA Subsidy Fight

This proposal is not an isolated idea but is strategically timed, directly linked to the issue that triggered the government shutdown.

1. Enhanced ACA Subsidies Are Expiring

At the heart of the congressional impasse is the future of enhanced ACA premium tax credits, which were expanded during the pandemic and are set to expire at the end of this year. These subsidies have helped approximately 24 million Americans significantly afford their coverage. Without renewal, experts estimate that monthly premiums for those purchasing insurance on the ACA marketplace could double or more.

2. Opposing Stances in Congress

Democrats have demanded an extension of these enhanced ACA subsidies as a prerequisite for voting on funding bills to reopen the government.

Republicans have insisted that Congress must first pass a “clean” funding bill to reopen the government, and only then should they discuss policy issues, including healthcare subsidies.

Mr. Trump’s proposal is viewed as a tactic to break the stalemate, offering a complete alternative to the current subsidy system while diverting focus away from the subsidy extension. However, senior Republican officials, including Treasury Secretary Scott Bessent, have already confirmed that Trump’s direct payment idea will not be formally introduced to the Senate until the government funding issue is resolved.

III. Analyzing the Impact and the Opposing Arguments

The proposal immediately garnered support from fiscally conservative Republican lawmakers and drew sharp criticism from Democrats and healthcare experts.

1. Arguments in Support (From Republicans)

Increased Individual Choice: Supporters argue that sending money directly to consumers empowers them. Instead of being locked into specific ACA plans, individuals could use the funds to purchase other types of insurance (including potentially less comprehensive, lower-cost plans) or contribute to an HSA.

Curbing “Fat Cat” Insurance Profits: Trump’s central argument is that the current system enriches insurance companies. Giving the money directly to the people, the argument goes, would foster competition and force insurers to offer better products at lower prices to attract customers.

Promoting Health Savings Accounts (HSA): Channeling funds into HSAs—tax-advantaged accounts used to pay for qualified medical expenses—is seen by some as a way to encourage greater consumer accountability and control over healthcare decisions.

2. Counterarguments and Concerns (From Democrats and Experts)

Risk of Losing Coverage: This is the most significant concern. The current ACA subsidy system is designed to ensure low-income individuals can afford comprehensive coverage that adheres to pre-existing condition protections. If the subsidy is converted into a cash payment or a fixed lump sum, it may be insufficient to cover an equivalent comprehensive plan, potentially leading to millions of people, especially the elderly and those with chronic conditions, facing skyrocketing premiums or losing insurance altogether.

Destabilizing the ACA Market: Experts warn that if healthier individuals opt out of the ACA market to take the cash or buy less comprehensive plans, the remaining pool would be sicker, driving up costs for the ACA marketplace and creating a “death spiral” that could lead to market collapse.

Lack of Concrete Details: To date, the proposal remains an idea floated on social media. No specific bill or detailed structure has been presented to explain how the payments would work, what the exact amount would be, and most importantly, how it would protect core ACA rules, such as prohibiting denial of coverage for pre-existing conditions.

Legislative Hurdle: For this plan to become law, it would need to pass both the House and the Senate, an unlikely scenario given the current deep political division, particularly with Democrats controlling the Senate.

IV. Technical Analysis: How Subsidies Currently Work

To understand the change proposed by Trump, one must look at how the ACA subsidies are currently structured:

-

Current System: Premium tax credits are sent directly to the insurance company (in most cases). The enrollee then pays only the remaining balance of the premium. This ensures immediate financial relief and guarantees that the insurance remains active.

Trump’s Proposal: Send the subsidy amount directly to the individual. The individual then decides how to spend that money on insurance or other healthcare expenses.

The difference lies in the certainty of sustained coverage. The current system locks the subsidy money into the purchase of insurance, whereas the new proposal turns it into a general income supplement or grant, running the risk that the individual may use the funds for other purposes and be unable to afford the full premium.

V. Conclusion: Strategy vs. Genuine Healthcare Reform?

President Donald Trump’s proposal to send Obamacare subsidies directly to Americans is a strategic move designed to reshape the healthcare debate and exert pressure on Democrats during the government shutdown fight.

While framed as a simple, pro-consumer solution, the proposal is thin on specific details and faces immense legislative hurdles. Without strict regulatory provisions to ensure people can still afford comprehensive, low-cost coverage, the plan could introduce significant volatility into the individual health insurance market and risk jeopardizing coverage for millions.

For now, the focus remains on resolving the government shutdown. Any major healthcare reform plan, including this one, will likely have to wait until Congress restores normal operations.

News

The Mountain Whisper: Six Years After a Couple Vanished in Colorado, a Fallen Pine Tree Revealed a Single, Silent Stone

The Rocky Mountains of Colorado possess a severe, breathtaking grandeur, offering both profound beauty and relentless danger. For those who…

The Ghost Pacer: How a Hiker Vanished in the Redwoods, Only for Her Fitness Tracker to Start Counting Steps Nine Months Later

The Redwood National Park is a cathedral of nature, a place where the trees stand like silent, ancient guardians, scraping…

The Haunting of the Sisters: How a Lone Discovery in an Idaho Forest Three Years Later Revealed a Silent Terror

The woods, especially the vast, ancient forests of Idaho, hold a unique kind of stillness. It’s a quiet that can…

The Locker Room Ghost: A Demolition Crew’s Routine Job Unlocks the Thirteen-Year Mystery of a Vanished Teen

The year was 2011, and the world seemed full of possibility for sixteen-year-old Ethan Miller. A bright, quiet student with…

The Ghost Kitchen: How a Missing Food Truck and a Routine Drone Flight Unlocked a Seven-Year-Old Mystery

Food trucks represent a certain kind of American dream: mobile, entrepreneurial, and fueled by passion. For Maria and Tomas Rodriguez,…

The Ghost Road Trip: Seven Years After a Couple Vanished, a Stranger’s Discovery Unlocked a Tragic Mystery

The open road holds the promise of freedom, adventure, and new beginnings. When Sarah Jenkins and David Chen decided to…

End of content

No more pages to load